Fractal Gaming Group AB (publ) (STO:FRACTL) shares have retraced a considerable 28% in the last month, reversing a fair amount of their solid recent performance. The last month has meant the stock is now only up 8.3% during the last year.

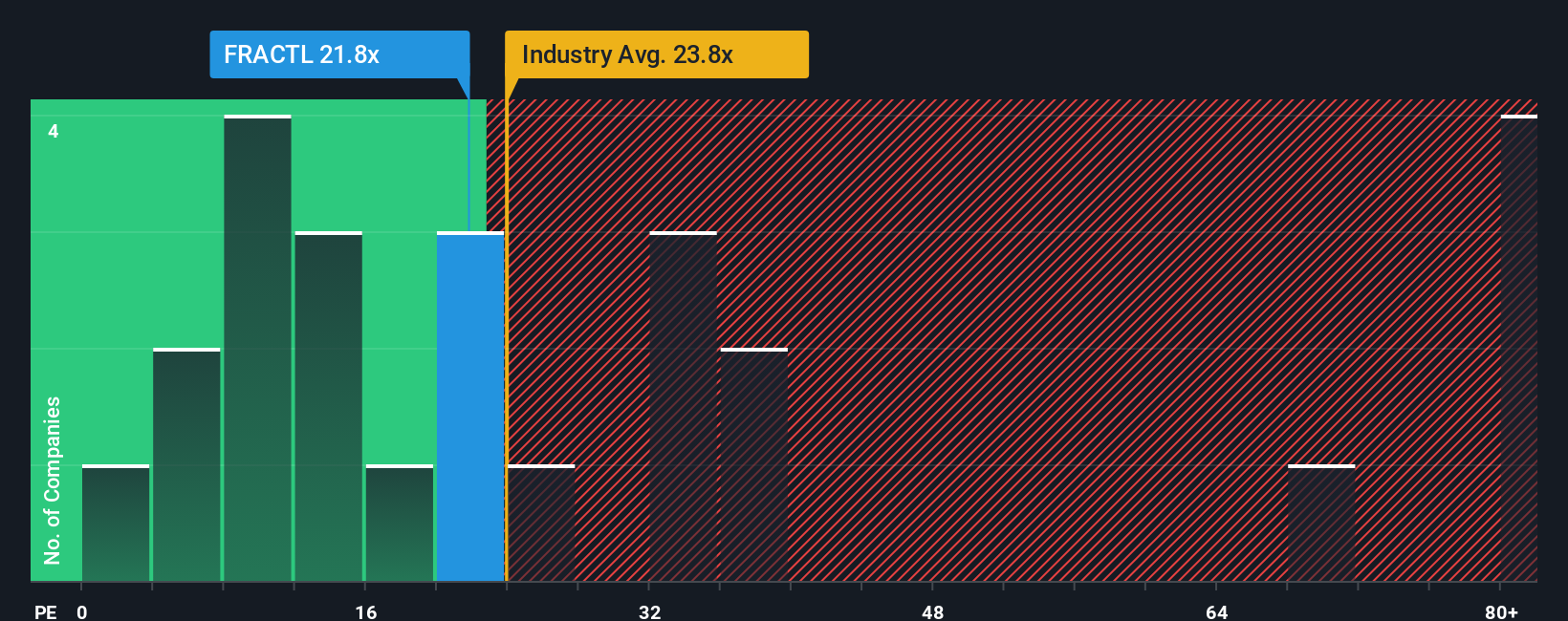

In spite of the heavy fall in price, it’s still not a stretch to say that Fractal Gaming Group’s price-to-earnings (or “P/E”) ratio of 21.8x right now seems quite “middle-of-the-road” compared to the market in Sweden, where the median P/E ratio is around 24x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Fractal Gaming Group could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Fractal Gaming Group

Want the full picture on analyst estimates for the company? Then our free report on Fractal Gaming Group will help you uncover what’s on the horizon.

What Are Growth Metrics Telling Us About The P/E?

There’s an inherent assumption that a company should be matching the market for P/E ratios like Fractal Gaming Group’s to be considered reasonable.

Retrospectively, the last year delivered a frustrating 8.1% decrease to the company’s bottom line. Unfortunately, that’s brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Therefore, it’s fair to say that earnings growth has been inconsistent recently for the company.

Turning to the outlook, the next three years should generate growth of 8.6% per annum as estimated by the sole analyst watching the company. That’s shaping up to be materially lower than the 18% each year growth forecast for the broader market.

With this information, we find it interesting that Fractal Gaming Group is trading at a fairly similar P/E to the market. Apparently many investors in the company are less bearish than analysts indicate and aren’t willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Key Takeaway

Fractal Gaming Group’s plummeting stock price has brought its P/E right back to the rest of the market. We’d say the price-to-earnings ratio’s power isn’t primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We’ve established that Fractal Gaming Group currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. This places shareholders’ investments at risk and potential investors in danger of paying an unnecessary premium.

Many other vital risk factors can be found on the company’s balance sheet. You can assess many of the main risks through our free balance sheet analysis for Fractal Gaming Group with six simple checks.

Of course, you might also be able to find a better stock than Fractal Gaming Group. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.